Over the next few weeks, we’ll share our views of the top three trends to watch for in the U.S. solar market (focusing on the PV market; apologies to the solar thermal folks reading). This week, we look at the first trend: soft cost reduction. It’s no secret that module prices have plummeted by 75% or more over the past three or four years. With module prices likely continuing to drop in 2013 as the industry works through chronic excess capacity, that will no longer be big news.

Lowering prices may mean more struggles for manufacturers and their suppliers, but even if module prices drop another 10% or 20% in 2013, it will hardly make a dent in end-customer solar system costs, particularly in the residential market. This is because the cost of solar is now significantly driven by soft costs.

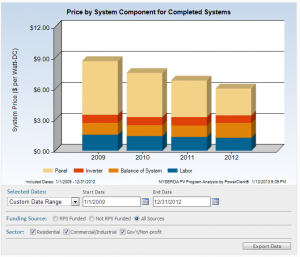

Module prices, which three or four years ago made up 50% or more of total system costs for residential customers, are now often less than 25% of total system costs. Soft costs have barely budged in absolute terms, and have increased from 25% or so of system costs just a few years ago to close to half of system costs today.

“Soft costs” are an often poorly defined amalgamation of costs associated with bringing a solar system online. The term is usually defined as all non-hardware costs, including:

- Sales tax

- Installation labor

- Permitting costs

- Incentive application costs

- Interconnection costs

- Installer profit

- Customer acquisition costs

As illustrated in the chart below, installation labor has been trending down slowly but steadily for years as installers capture economies of scale, hardware becomes easier to install, and installers climb the learning curve. Meanwhile, other soft costs have remained stubbornly high. Soft costs are also difficult to measure. Any line item on the customer invoice can involve a mark-up, and to truly understand soft costs it is necessary to dissect installer organizations to a very granular level.

There are a number of efforts currently underway to study and reduce soft costs. The National Renewable Energy Laboratory and Lawrence Berkeley National Laboratory recently released a study benchmarking solar soft costs based on 2010 data. Reports like this help us understand where the opportunities for cost reduction lie. The team is now updating this study to reflect current data.

In addition, the Department of Energy SunShot initiative has a significant focus on soft cost reduction. The SunShot program managers recently announced a second round of funding for the Rooftop Solar Challenge, which seeks to “make installing rooftop solar photovoltaics (PV) easier, faster and cheaper for homeowners and businesses.”

And it isn’t just the federal government getting into the game. The State of New York is providing $30 million under the Solar Market Acceleration Program – Solar MAP – with a goal of funding soft cost reduction strategies.

At Clean Power Research, we like to think of ourselves as leaders in the space of soft cost reduction. Our Clean Power Estimator® and QuickQuotes™ products have been helping companies lower the costs of customer acquisition for many years. Our PowerClerk® software has dramatically reduced the administrative costs associated with incentives across many states, and we’re currently expanding the PowerClerk lineup to include capabilities that will help reduce the costs associated with interconnection.

We’re confident that with the renewed focus from government and industry, we’ll see dramatic reductions in solar soft costs over the next few years.